For the third and final article of our WIRE series focusing on Residential Mortgage Backed Securities (RMBS) and Asset Backed Securities (ABS) we wrap it up with their performance.

Having gone through the key characteristics of RMBS notes and some of the key technical terms, we are looking now at how these notes have generally performed over time. Given hundreds of series of notes have been issued over the years, we have limited

our focus on tranches that our clients have purchased and are still outstanding.

Since 2009, when the GFC ushered in a new regime of understanding and rating these kinds of securities, over 3,400 have been issued. The oldest transaction was issued in 2014 by AMP Bank and we currently have in our custody 163 different series of RMBS

and ABS notes with a total issued amount in excess of AUD1.8bn.

1. Rating performance

Credit ratings are designed to provide a relative indication of risks based on a theoretical stress scenario. The highest rating, AAA, is assigned to securities that are expected to survive the harshest of stress scenarios. At the other end of the spectrum,

a rating of B would only survive a modest stress environment. As it has been well reported, credit rating agencies faced significant heat as a result of many structured finance transactions defaulting during the GFC, even though their ratings implied

they would have survived (as an aside, these securities were issued primarily in the US and significantly more complex than the RMBS or ABS securities we have been discussing in this edition of the Wire).

As a result of the GFC, credit rating agencies have fundamentally revised their rating methodologies to ensure they are a lot more robust and can stand up to scrutiny a lot better. In practice, credit rating agencies have taken a far more conservative

approach and it is widely accepted that RMBS ratings incorporate a certain level of conservatism compared to ratings issued for corporates or financial institutions.

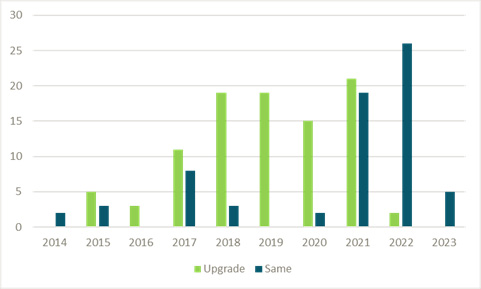

The graph below shows, for all the rated notes we have in our custody, how their current ratings are compared to where the same notes were rated on issue.

Of these 163 series, 95 have been upgraded by at least one notch (on average, the upgraded tranches are rated close to three notches higher, with the largest upgrade for the Liberty 2019-2 E given its current rating of Aa1, compared to an initial rating

of Ba2). Importantly, not a single tranche is currently rated lower than its original rating.

Source: S&P Global Ratings, Moody’s Investors Services, FIIG Securities

Interestingly, an overwhelming majority of transactions issued between 2017 and 2020 have experienced an upgrade since issuance and the 2021 vintage is on track to maintain this trend. The rate of upgrade naturally drops materially for the 2022 vintage,

given rating agencies will typically want to see a meaningful track record of positive performance before lifting a rating.

As it stands, 58% of the 163 transactions have so far experienced an upgrade, with an average rating uplift just below three notches, which talks to a very strong performance across the asset class (but also our thorough selection process).

2. Principal amortisation

As we discussed in the second article, RMBS transactions are structured to initially have the most senior tranche receive all the principal repayments and, provided certain tests are met, then principal repayments will be allocated on a pro-rata basis.

These tests that determine this change in payment allocation are effectively a proxy for performance against expectation. If a test is not met, it could be because the transaction doesn’t perform as expected.

There are generally three triggers:

- The payment date has to be at least two years after the issue date – this clearly is independent of performance;

- The credit support for the most senior tranche should be more than a pre-determined level – this is partly tied to performance;

- Arrears should be below a certain threshold – completely tied to performance.

Taking the second test above, there are generally two reasons this test is not met: 1) the speed at which underlying mortgages are prepaid early is lower than originally anticipated, or 2) there is a relatively high level of default. In our experience,

the second scenario is highly unlikely and would happen only if high arrears have been previously observed. We note that the level of losses on Australian RMBS remains extremely low and have generally been covered by a combination of claims on lenders’

mortgage insurance and excess spread.

Source: Bloomberg, FIIG Securities

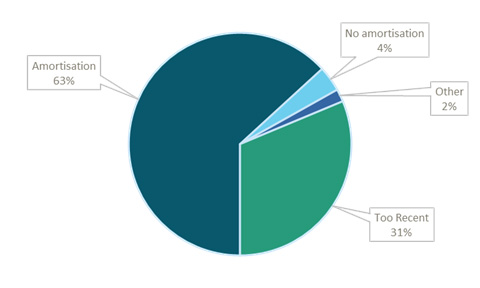

Of the 163 series of notes in our custody, 103 notes are receiving ongoing amortisation, meaning they are supporting transactions that are performing at least in-line with original expectation. Of the remaining 60, 51 were issued less than two years ago

(meaning that, irrespective of performance, they wouldn’t be eligible for amortisation), and six were structured not to receive any ongoing amortisation (rare but some are structured that way). Which leaves only three tranches (across two transactions)

which are currently not receiving amortisation (having previously received some).

These two transactions are Torrens 2014-2 and Resimac Bastille 2018-1NCX. The absence of amortisation for the former is linked to the Class D notes having been paid down to their floor level (of AUD1.185m). We expect this transaction to be cleaned up

in May 2024. The Resimac transaction no longer pays amortisation because the total outstanding amount across all tranches is now less than 20% of the original aggregate amount of notes issued, which would trigger the clean-up call. We currently expect

this transaction to be called over the coming months, accounting for the original assumption of a call in August 2023.

3. Conclusion

The above two reference points are only two of many areas that can be closely scrutinised when assessing if a RMBS transaction is performing to expectations or not. Other areas that are good to follow include how arrears evolve over time, how the weighted

average loan to value ratio decreases over time, net losses on foreclosed loans (where relevant).

In fact, monthly reports are generated that provide a lot of granular information on the underlying portfolio, which provides sufficient indication to determine if the loans are behaving in line, better or worse than expected. While over the last few

years, the residential housing loan market has experienced ups and downs (all within reason), the performance of Australian RMBS transaction has remained very solid and demonstrates the robustness of these structures.